Hi everyone – as I normally do each month, this is my eToro review for April. I

** If you don’t have an eToro account – you can set one up here! **

** Already have an eToro account? Check out my profile! **

67% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money.

Note that this does not apply to US Users and eToro USA LLC does not offer CFDs.

Goal comparison

- Copiers = 29 (-2 Copiers)

- Followers = 6% increase YTD

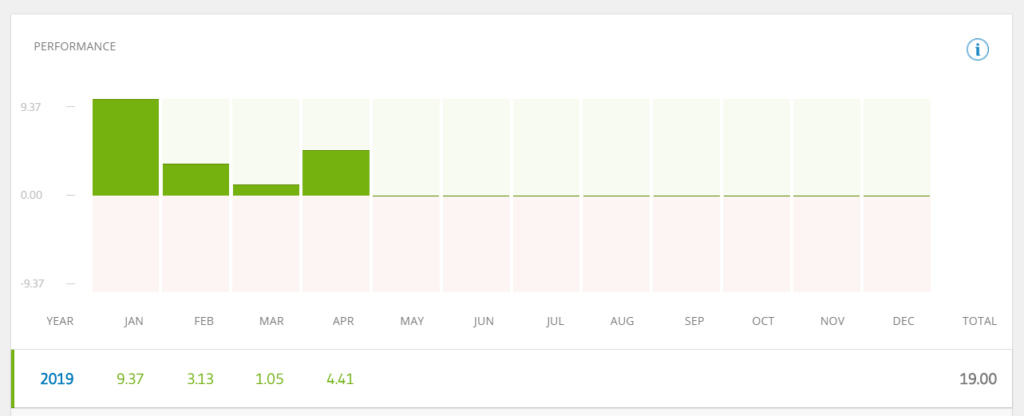

- Portfolio growth = 19.00% increase YTD

- S&P comparison = beat for YTD (17.51% vs 19.00% source: investing.com)

- Realised Profit = 0.07%

- AUM = 83% increase

- April Risk Level = 3 (4 last month) – 19% portfolio gain for 2019 and a risk level of 3 is a great result

- Monthly updates = Complete

So my aim of keeping to my etoro trading goals is looking on track. I’ve hit all my targets for the month and look forward to what May 2019 has in store for us. Our portfolio growth is still growing and beating the SP500 which is a great benchmark for success. Below, you can see that we have several positions in great profit, ready to be taken when the market is right.

eToro April Portfolio overview

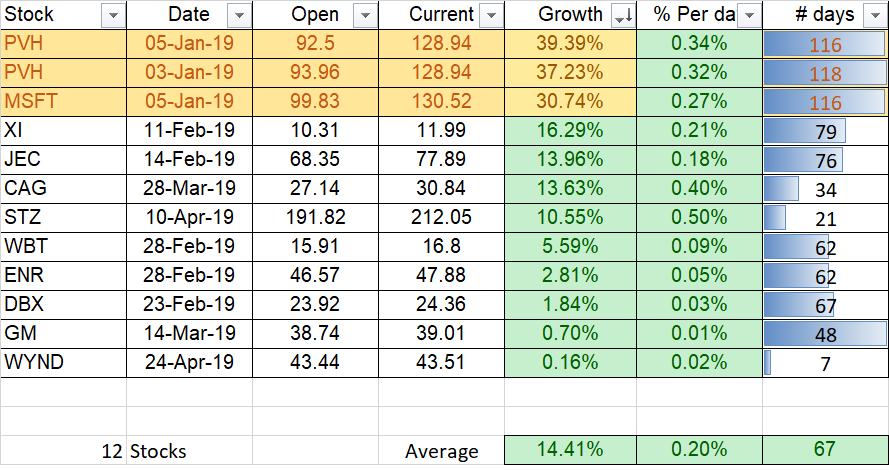

Overall, my eToro portfolio has had a great start to the year. The new positions I’ve opened this year have had a great start. As mentioned in the previous month, I’ve begun focussing my stocks on strong US stocks that will provide great profits over the coming months/years. Below is a snapshot of what stocks I’ve opened and haven’t closed yet in 2019.

Current 2019 Open eToro stock positions

As you can see, $PVH is still leading the charge in growth, with $MSFT having a fantastic month thanks to a stellar earnings report. Bringing it to nearly 12% in one month alone.

Portfolio Growth and dates

- 5% – Achieved January 8, 2019

- 10% – Achieved February 6, 2019

- 15% – Achieved March 22, 2019

- 20% –

The 30% Sunshine Club

These are the stocks that I’ve bought in 2019 and are currently making our portfolio look good! These stocks are laying on the beach in the sunshine – hitting 30% profit since being bought.

- $PVH = 39.39%

- $PVH = 37.23%

- $MSFT = 30.74%

It’s great to see all open 2019 positions in positive territory. Over the coming weeks and months, we can take these profits and add it to our realised profit growth for 2019.

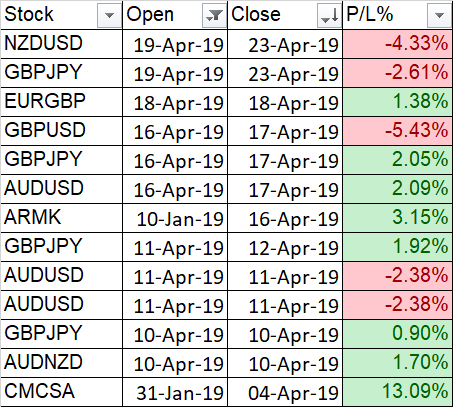

Closed eToro positions

I have taken a different reporting approach for my 2019 closed positions. I realised, if I’m only showing stocks I’ve open in 2019, then I should only be reporting on those same stocks which I have closed in 2019. So all the stocks I’m reporting on were executed in 2019.

March has been a mixed bag of closed positions. Some really strong positive territories and a bad forex venture. I decided to go back to the eToro virtual account for my forex training and fine tune what I’ve learned. This will allow me to take small profits consistently, adding up over the course of a year to help boost our realised profit.

New Stocks added to my eToro portfolio

With analysis help from @Tipranks

Constellation Brands (STZ)

A top-rated cannabis play

If you are looking for cannabis exposure but with limited risk, look no further. Drinks giant Constellation Brands is the owner of popular drinks brands like Corona and Modelo beer.

However, it also boasts a 38% stake in Canadian cannabis giant Canopy Growth Corp following a massive $4 billion investment in 2018. Although the size of this investment has made some investors wary, the deal has its supporters. I am definitely one of them. Cannabis is a hugely exciting market right now. According to Cowen & Co’s Vivien Azer — aka the first pot analyst — U.S. marijuana sales are set to reach about $80 billion by 2030. Currently, U.S. legal and illicit sales total at least $50 billion.

That’s on top of an estimated 12 billion Canadian dollars in revenue by 2025, for both recreational and medical use, and $31 billion by 2025 in the 43 countries that have legalized medical cannabis or are likely to do so.

But it is still early days

That means that there is still a significant degree of risk involved. STZ offers a unique balance between exposure and stability. Pivotal Research analyst Timothy Ramey writes

“We are convinced that CGC is the best way to play the rapidly growing cannabis market and investors should begin to fully reflect that value and CGC’s prospects, rather than penalizing STZ for the cash carrying costs of the investment.”

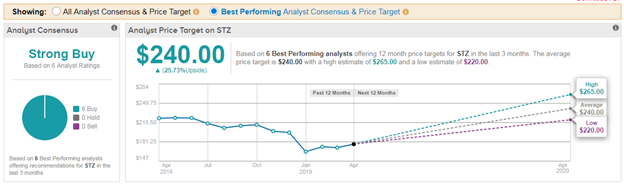

As a result he concludes on April 4: “This makes STZ a truly compelling BUY.” His $265 price target indicates 38% upside potential from current levels.

Right now the consensus on STZ from the Street is Strong Buy. And even better, if we zoom in on only top-performing analysts they are showing 100% support for STZ. That’s with an average price target of $240 (26% upside potential).

A stellar earnings report

Also in the stock’s favor comes the company’s recent earnings report which left a positive impression on analysts and investors alike. While beer sales came in strong, wine sales proved disappointing. Gladly however, Constellation has already resolved this, by announcing a divestment of lower priced wine and spirits brands. It will sell 30 of its lower-priced wine and spirits brands to Gallo for about $1.7 billion.

While the sum may be less than some hoped, Constellation nonetheless believes the move “re-shapes” its portfolio and positions it on a “clear path” to double-digit core earnings growth.

Following the announcement, Wells Fargo’s Bonnie Herzog gave this positive review of the decision:

“Although the proceeds are less than our expectations (we assumed closer to ~$2.3B based on our scenario analysis), we view this transaction favorably since it should remove an overhang that has been weighing on the stock since October and creates value as it repositions STZ’s wine portfolio into a faster growing (~MSD growth) and higher margin (~30% EBIT margin) business”.

Bonnie Herzog – Wells Fargo

Meanwhile Jefferies’ Kevin Grundy reiterated his take on STZ as a ‘top pick’ and ramped up his price target from $255 to a Street-high $267. “The solid print/guidance, strong Nielsen data (beer +11.1% in latest 12-wks), and an exciting innovation pipeline should help put the bear thesis on hold for now, in our view” he explained.

Wyndham Destinations $WYND

Wyndham Destinations sells its vacations one piece at a time. The company operates a vacation ownership (VO) operation with over 220 locations across 110-plus countries.

Last June, management spun out its hotel business, Wyndham Hotels & Resorts (WH), to create the biggest pure-play in the VO (or timeshare) business.

That scale is one of the company’s biggest competitive advantages. By most measures, Wyndham is twice as large as competitors like Hilton Grand Vacations (HGV) and Marriott Vacations Worldwide (VAC).

By nature, the VO business also offers investors stable and consistent growth. Through annual dues and other fees, Wyndham says that 75% of its annual revenue is both recurring and predictable.

Analysts Bullish on the Future

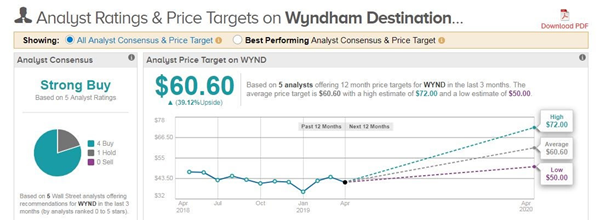

Four of five analysts with recent coverage on the stock rate it a Buy, while the other has a Hold rating. The average analyst price target on the company is $60.60, which represents 39% upside from current levels.

Top-rated analyst, Harry Curtis of Nomura, recently cited two ways that Wyndham can create value for investors:

“Take WYND Private: In the wake of Bluegreen’s (BXG) privatization due to persistently low valuation, we see this as a potential avenue for WYND to generate value for shareholders given the stock’s sub-6x 2020E valuation.

Divestitures: We believe that WYND would consider selling its RCI exchange business given its LSD growth trajectory. A sale may be valued at +$2bn, with net cash proceeds being returned to shareholders.”

In the meantime, Curtis notes that shares have an attractive 15% free cash flow yield, based on 2020 projections.

Earnings and Dividend Moving Higher

The company will announce quarterly results on May 1 and management has met or exceeded the consensus analyst profit estimate seven of the past eight quarters. Wyndham is expected to earn $0.90 a share in the first quarter, up from $0.84 in the previous year, on $918.9 million of revenue.

One key metric to watch each quarter is tour volumes, which is how the company generates new sales leads. Management has recently replaced underperforming U.S. sales locations with new tour offices, which are expected to bear fruit throughout 2019.

Dividends

Dividends are an important part of the story and Wyndham. Management started paying a quarterly dividend of $0.41 a share following the spin-off, which was raised to $0.45 (4.1% yield) in March.

The company can comfortably cover the payout 3x with expected 2019 earnings of $5.32 a share. Management has also returned capital to investors through stock buybacks, which exceeded $100 million each of the past two quarters.

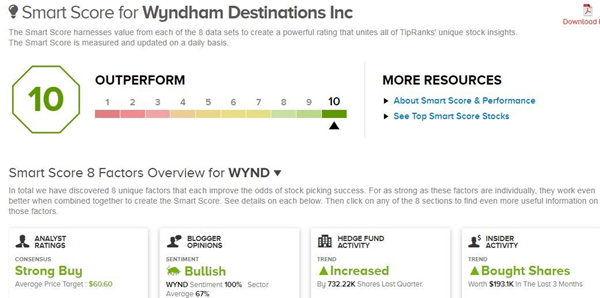

Finally, the stock has a Smart Score of 10/10 on TipRanks. This new proprietary metric utilizes Big Data to rank stocks based on 8 key factors that have historically been a precursor of future outperformance.

In addition to the positive aspects mentioned already, Smart Score says that Wyndham has favorable insider activity, in addition to positive blog and investor sentiment.

Final thoughts on my eToro April Review

April 2019 has been a decent month for my eToro portfolio – a great month for stocks and focusing on the rest of 2019. We’re beating or on par for most of my 2019 eToro goals so I’ll be keeping a close eye on the remaining months.

Remember to Stock Up with Joe

Also, if you like the stats above, check out Simply Wall St – they provide some great analysis into thousands of stocks.

[…] quick scheme and more into buying and holding. But for those who believed and stayed have enjoyed a 19% portfolio growth from Jan to April alone! Beating out the S&P500 for every month this […]

It’s hard to find knowledgeable people on this topic, but you sound like you know what you’re talking about! Thanks