Hi everyone – as I normally do each month, this is my eToro review for May. I

** If you don’t have an eToro account – you can set one up ! **

** Already have an eToro account? Check out my profile! **

67% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money.

Note that this does not apply to US Users and eToro USA LLC does not offer CFDs.

Goal comparison

- Copiers = 28 (-3 Copiers)

- Followers = 6.2% increase YTD

- Portfolio growth = 14.98% increase YTD

- S&P comparison = beat for YTD (14.98% vs 9.78% source: investing.com)

- Realised Profit = 1.22%

- AUM = 88% increase

- April Risk Level = 3 average (4 Max)

- Monthly updates = Complete

Looks like I’m hitting my goals in every category except for copiers. Our portfolio growth is still growing and beating the SP500. This is a great benchmark for success.

eToro Review – May Portfolio

My eToro portfolio was affected during May. This is a result of the Tariff Wars. This has affected my portfolio with connections in China and Mexico. I’ve begun focussing my stocks on strong US stocks that will provide great profits over the coming months/years. Below is a snapshot of what stocks I’ve opened and haven’t closed yet in 2019.

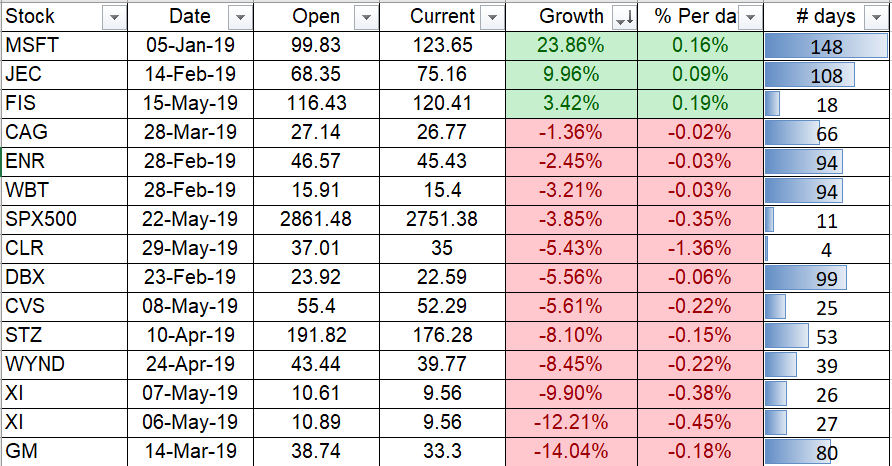

Current 2019 Open eToro stock positions

As you can see, there is a lot of red. Most of these stocks were victims of the trade war. $MSFT is still out in the lead. There are still some very promising stocks within this portfolio, just itching to break out!

Portfolio Growth and dates

- 5% – Achieved January 8, 2019

- 10% – Achieved February 6, 2019

- 15% – Achieved March 22, 2019

- 20% – Achieved May 17, 2019

- 25% – Coming soon!

- 30% – Coming soon!

The 30% Sunshine Club

Unfortunately, none of our open stocks are in this exclusive club at the moment. These stocks are laying on the beach in the sunshine. Since being bought, they have climbed to 30% in profit. Hopefully, we’ll add more this coming month.

Closed Stocks in the Sunshine Club

None at the moment

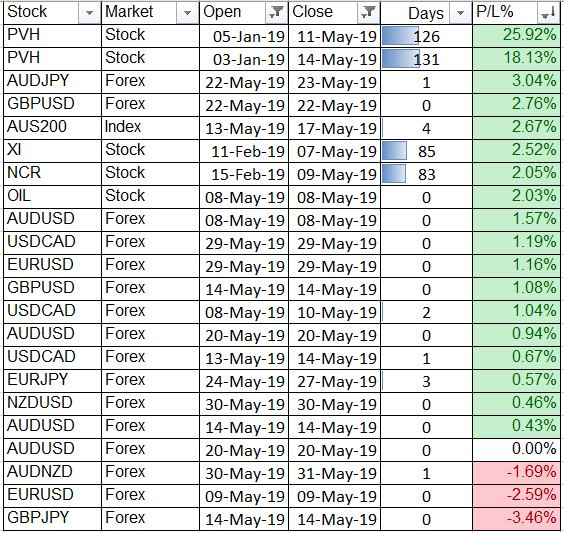

eToro May Review Closed positions

I have taken a different reporting approach for my 2019 closed positions. I realised, if I’m only showing stocks I’ve open in 2019, then I should only be reporting on those same stocks which I have closed in 2019. Each stock has been bought and sold in 2019 only.

May saw a positive turn for closed positions. I closed 22 positions this month. 18 in positive territory, 1 broke even, and 3 loses.

73% of my trades this month were Forex. 75% of those trades were closed in positive.

As you can see, I closed out my $PVH holdings with a decent profit. A good result considering that lost about 15% a week or two after due to the Tariff War with China and a poor earnings report. Positive territory for my eToro May Review.

New Stocks added to my eToro portfolio

With analysis help from @Tipranks for my eToro May Review.

Continental Resources (CLR)

The first new purchase to boost our exposure to the energy patch. Continental Resources is an oil (60% of business) and natural gas (40% of business) exploration firm with sizable assets in the Bakken field in North Dakota and Montana, which account for more than 40% of its total 1.9 million net reservoir acres.

One big competitive advantage the company has relative to its peers is low production costs. Continental claims that it can post break even cash flow, even if crude oil dips below $40 a barrel. This leverage allows management to generate $325 million of incremental annual cash flow for every future $5 increase in the price per barrel of oil.

The company posted better-than-expected quarterly results back in April. Continental earned $0.58 a share in the first quarter, as revenue fell fractionally from the previous year, to $1.12 billion.

Management

Management is looking to build upon this momentum and is projecting 12.5% average annual production growth over the next five years. In the meantime, the company’s balance sheet has been improving. Net debt is expected to fall to $5 billion this year.

Analysts Have 100% Buy Ratings. The stock has a consensus Strong Buy rating from the analyst community and the average price target of $58.57 from seven active analysts represents 54% upside potential.

Following the latest quarter, analyst Betty Jiang of Credit Suisse commented:

“CLR delivered a solid ~2.5% oil beat vs Street with EBITDX ~8.5% ahead on higher volumes and better cash costs. Despite concerns around elevated spending, 1Q capex can be rationalized by a higher level of activity in the Bakken (which translated into production) and mineral spend running ahead of the budgeted quarterly run rate. Adjusted for the latter, we see 1Q capex at just ~3.5% above Street. With accelerated development pace in both Bakken and SCOOP, we believe CLR is poised to meet or exceed the high end of the FY production guidance range. Cash flow can further improve with potentially lower per-unit costs which were noted in the release to see room for positive adjustment later in the year.”

CEO is Largest Holder and Buying More

People sell for a number of reasons – if they’re buying a stock it’s for only one. It’s going to go up. Chief Executive Officer and Chairman Harold Hamm is the largest holder of Continental, controlling about 76% of the shares outstanding. Hamm has been putting his money where his mouth is lately, making three Informative Buys in the past quarter, worth nearly $80 million.

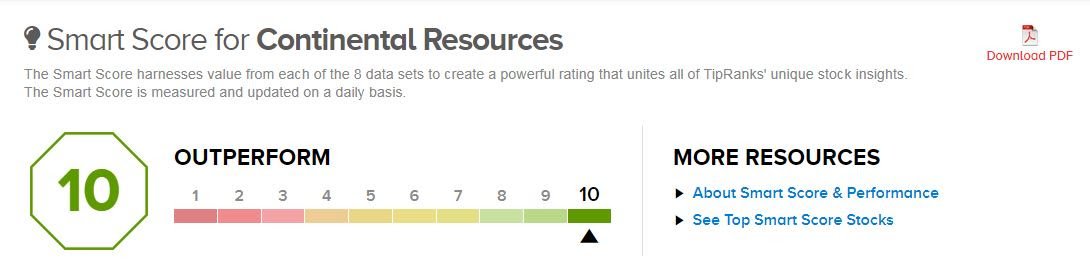

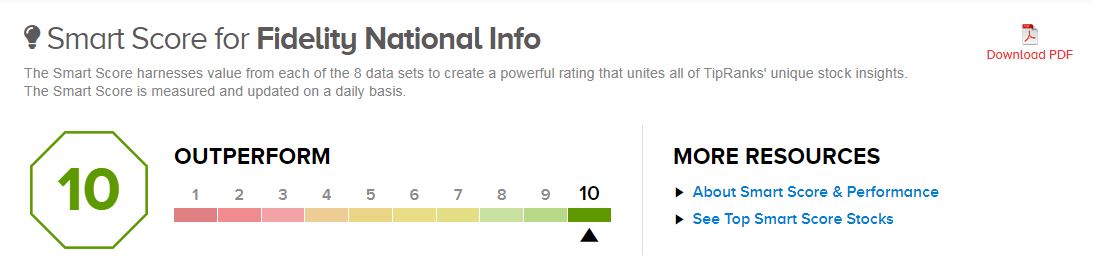

It’s also worth noting that the stock has a Smart Score of 10/10 on TipRanks. This new proprietary metric utilizes Big Data to rank stocks based on 8 key factors that have historically been a precursor of future outperformance.

In addition to the positive aspects mentioned already, Smart Score says the company has positive sentiment from hedge funds, financial bloggers and recent news.

New Addition: Fidelity National (FIS)

Next in my Etoro May Review – You may not be familiar with the name, but there’s a good chance that Fidelity National touches your money on a daily basis. The company is the leading processor of payments and other transactions for banks and various financial institutions.

After more than 50 years in business, Fidelity National counts more than 20,000 customers across 130 countries. The company processes billions of transactions annually that helps move $9 trillion around the globe.

Management posted better-than expected quarterly results on April 30. Fidelity National earned $1.64 a share in the first quarter, as revenue fell fractionally, to $2.06 billion.

Company buy backs

The company bought back $400 million worth of shares in the quarter and has $2.28 billion remaining on its repurchase authorization. Fidelity National also pays a quarterly dividend of $0.35 a share (1.2% yield) that management raised earlier this year. June is the next payout.

Analysts See Further Upside Potential

In reaction to the quarter, top-rated analyst, Joseph Foresi of Cantor Fitzgerald raised his price target to $134, citing:

“We believe the company has the opportunity to accelerate revenue growth, improve margins and deleverage, which should have a positive impact on results and multiples. We continue to like FIS’s high visibility and recurring revenue business, which produces a steady stream of mid-singledigit annual revenue growth, which could be accelerated through a better selling environment, margin expansion, and taking market share.”

Foresi is rated #3 of the more than 5,000 analysts tracked by TipRanks. In total, 10 of 11 analysts with active coverage of the stock rate it a Buy, with one Hold. The average price target of $132 suggests 13% upside potential from current levels.

Merger Boosts Growth Potential

A significant portion of Fidelity National’s expected future growth is a result of a massive merger that management announced earlier this year.

Back in March, the company said that it would acquire competitor, UK-based Worldpay, assigning an enterprise value of $43 billion to the deal. Fidelity National is paying a mixture of cash and stock for the deal and will control 53% of the combined company.

Not competition

While Worldpay does compete with the company, its core competency is processing debit and credit card payments for merchants, while Fidelity National’s strength is the underlying software. As a result, management has identified another potential $500 million of annual cross-selling opportunities from combining the two customer bases.

Aided by the merger, consensus analyst estimates call for the company to average 20% earnings growth over the next three years. The stock is currently valued at 14.4x expected 2020 earnings of $8.13 a share.

In the meantime, the stock has a ‘perfect’ Smart Score of 10/10 on TipRanks. This new proprietary metric utilizes Big Data to rank stocks based on 8 key factors that have historically been a precursor of future outperformance.

In addition to the positive aspects mentioned already, Smart Score says that Fidelity National has improving sentiment from investors (both institutional and individual), in addition to financial bloggers.

New Addition: CVS Health (CVS)

Next up in my eToro May Review. An established name with stable growth and low P/E could be just what the doctor ordered. This market is white-hot, but is now experiencing increased volatility.

The company provides medical insurance to 22 million users through Aetna and covers pharmacy benefits for 92 million customers through Caremark. In addition, CVS Health treats patients directly through its network of over 1,100 Minute Clinics.

Earnings Momentum

Management combined all of those businesses and more into one solid quarterly report last week. The company earned $1.62 a share in the first quarter, which exceeded the consensus analyst estimate.

Revenue increased 35% from the previous year to $61.65 billion and also topped expectations. In addition to the solid results, CVS Health boosted its profit guidance for the second quarter, to $1.68 to $1.72 a share.

Not everything has come easy to the company in 2019. The healthcare sector has been hurt by the “Medicare for All” discussion and CVS Health took a $2.2 billion impairment on a previously acquired long-term care business earlier this year.

We were was encouraged to see that a cluster of six members of the company’s Board of Directors stepped up to buy the stock on the open market. Something that caught my eye during my eToro May Review.

Analysts Agree About Upside Potential

Unlike some names in the Smart Investor portfolio, CVS Health isn’t flying under the radar. The company has a market valuation north of $70 billion and 20 analysts maintain regular coverage.

One thing the analyst community does agree about is that the stock has considerable upside potential. The average price target of $72.76 offers nearly 32% upside potential from current levels.

Analyst predictions

Following the latest quarter, analyst Ricky Goldwasser of Morgan Stanley increased his forward estimates, citing:

“1) New Enterprise Modernization initiative to yield net savings of $1.5 billion to $2 billion by 2022. 2) Accelerated debt pay down, should bring leverage ratio down to 4.3x by 2H of calendar year, clearing the path to ~4x by next year and for investors to think more constructively on valuation. 3) Strategic asset review is under way.”

The stock is currently valued at just 8.3 times expected full-year earnings of $6.77 a share. This is a steep discount to the current market multiple of 17x and the average of the company’s peer group (11x to 12x).

As CVS Health integrates the Aetna acquisition and gets another couple of solid quarters under its belt, the shares deserve a double-digit multiple.

In the meantime, the stock has a Smart Score of 10/10 on TipRanks. This new proprietary metric utilizes Big Data to rank stocks based on 8 key factors that have historically been a precursor of future outperformance.

In addition to the positive aspects mentioned already, Smart Score says that CVS Health has improving sentiment from investors (both institutional and individual), in addition to news and financial bloggers.

Final thoughts on my eToro May Review

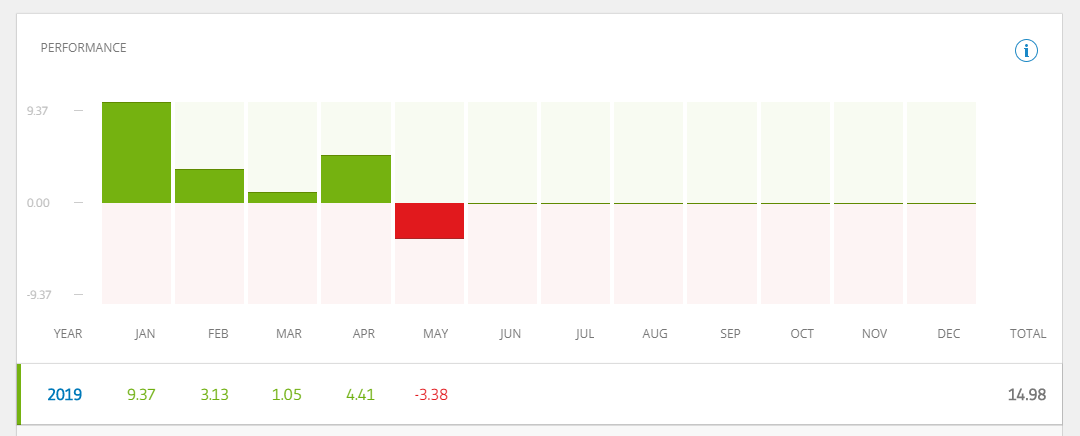

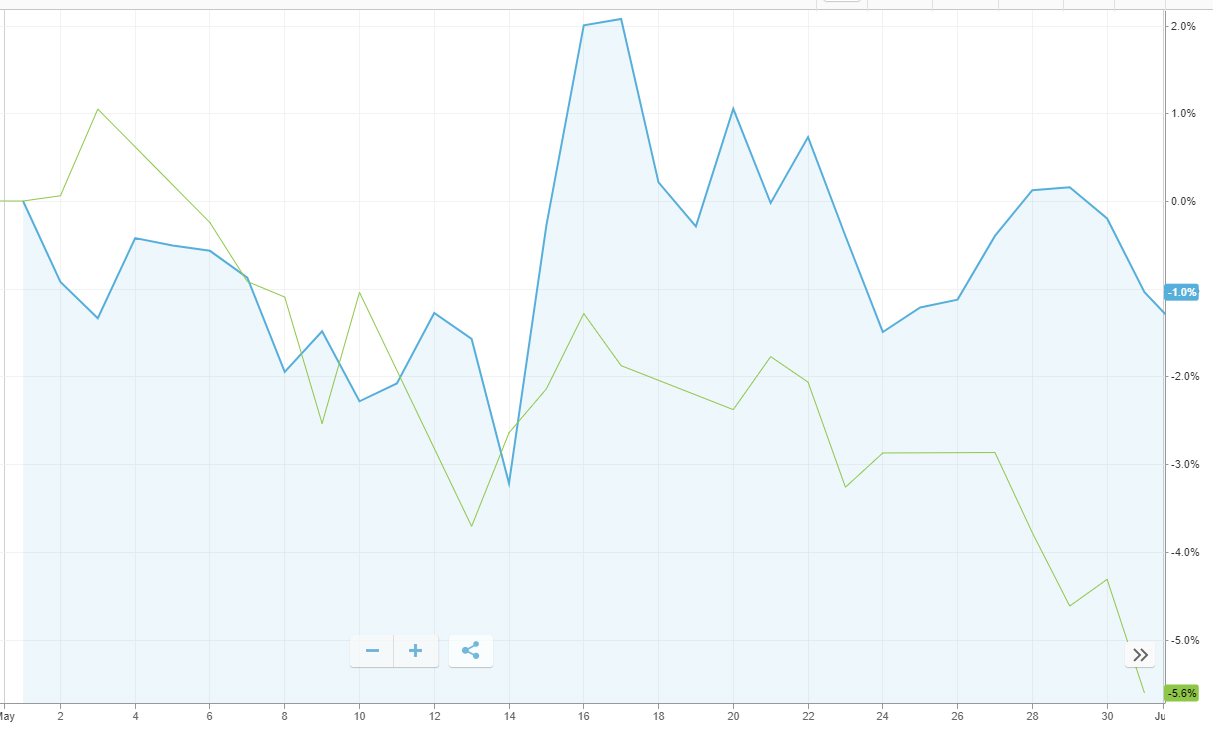

May 2019 was a difficult month. It was extremely volatile due to the tariff war and the cryptocurrency jump. Check out the comparison to the SP500 over the month – My portfolio is in blue and the SP500 in green. We’re beating or on par for most of my 2019 eToro goals so I’ll be keeping a close eye on the remaining months.

Remember to Stock Up with Joe

If you’re not sure where to start with your financial journey – get your finances in check with my Top 5 Personal FInance Books for beginners.

Also, if you like the stats above, check out Simply Wall St – they provide some great analysis into thousands of stocks.

Thank you for taking the time to read my eToro May review.

Disclaimer: Please note that some of the above links are affiliate links. They don’t cost you anything but I may receive an incentive if you click on it.

Please note that none of the above is financial advice. I have not taken into consideration any of your financial situation(s). Please do your own research when looking at the stock market and seek a licensed professional’s advice before committing.

eToro is a multi-asset platform which offers both investing in stocks and cryptoassets, as well as trading CFDs.

Please note that CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 67% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work, and whether you can afford to take the high risk of losing your money.

Past performance is not an indication of future results.

Cryptoassets are volatile instruments which can fluctuate widely in a very short timeframe and therefore are not appropriate for all investors. Other than via CFDs, trading cryptoassets is unregulated and therefore is not supervised by any EU regulatory framework.

eToro USA LLC does not offer CFDs and makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication, which has been prepared by our partner utilizing publicly available non-entity specific information about eToro.

I believe other website owners should take this internet site as an example , very clean and wonderful user friendly design.